GSE Recap/Release and Price Reflexivity

Will recent GSE common stock price action have any effect on the likelihood and terms of GSE recap/release?

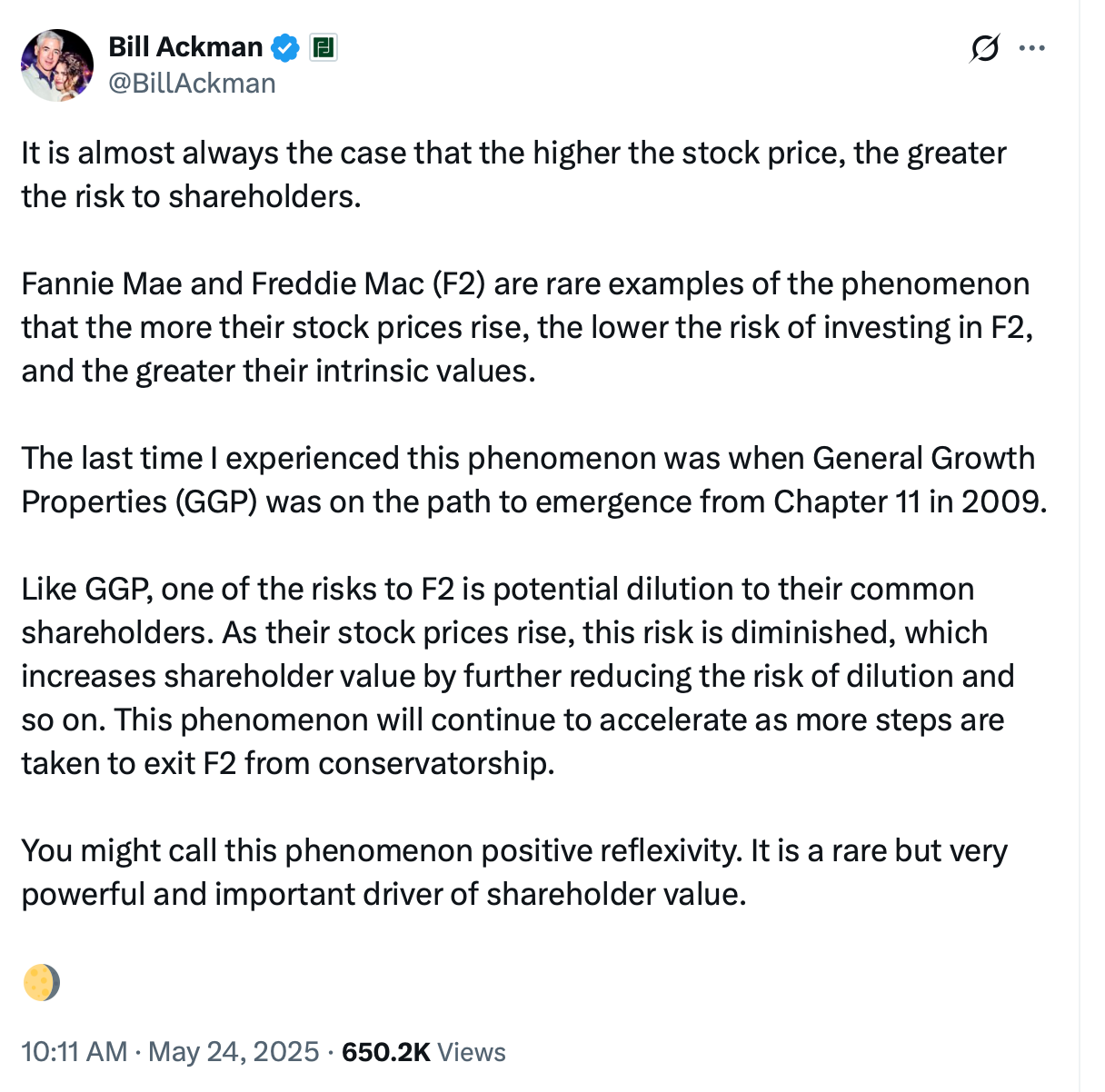

Bill Ackman posted this on X a few months ago:

Price reflexivity is a market concept first expounded by George Soros in "The Alchemy of Finance", published in 1987. In this work, Soros introduces his theory of reflexivity, which explains how market participants' perceptions and actions can influence asset prices, creating feedback loops that affect market dynamics.

It is a simple enough concept. One observes how markets are composed of many market participants who not only price assets individually through share purchases and sales, but observe other market participants doing so and are influenced by that market behavior.

In other words, “the market made me do it”.

Underlying this market reflexivity behavior is the great work done by Rene Girard, who observed that people are highly mimetic, and observe and copy what others are doing. It is the fundamental basis of social media. It is also a significant influence on market dynamics.

Girard posited that mimetic behavior creates societal conflict when multiple parties seek the same objective but are constrained by limited resources in achieving that objective. In markets, Soros observed that this mimetic behavior results in market activity that feeds back onto the market, further influencing market activity. Stock price action can affect the behavior of the issuers themselves as well as market participants.

So what does this have to do with GSE recap/release?

I note that over the last five trading days, Fannie Mae common stock (FNMA) is up almost 15%, and Freddie Mac common stock (FMCC) is up over 35%. All this goosed by a couple of media interviews by Treasury Secretary Bessent and FHFA Director Pulte.

Will this recent market performance by FNMA and FMCC have a reflexive effect upon the likelihood and terms of GSE recap/release?

In particular, one can imagine that if Treasury Secretary Bessent said in his next media interview that Treasury will convert all of its GSE senior preferred stock liquidation balance (SPS) into GSE common stock in connection with a GSE recap/release and totally dilute GSE common stockholders, that would crush the trading prices for GSE common stock.

Not a smart choice if Treasury wants to maximize the value of its GSE common stock holdings in forthcoming stock offerings.

Will this recent GSE common stock price performance have the reflexive effect of making Treasury SPS conversion less likely, and Treasury cancellation of SPS more likely?

One of the first principles of equity capital markets is that you don’t engage in behavior before an offering that damages the likelihood of a successful equity offering.

This is called “not crapping in your bed”. (Yes, investment bankers veer towards the school yard when searching for profundity).

Will Treasury Secretary Bessent and FHFA Director Pulte look at this recent common stock price action and be reflexively influenced by it?

* * * * *

As always, this substack provides investment analysis, not investment advice. Do your own due diligence.

Can you explain how and what will happen with the news that they plan on selling somewhere between five and 15% of their holdings. Would this be the government exercising their warrants, or would they be selling the senior preferreds ???how would all of this happen???