GSE Recap/Release: Add A "Contingent Value Receipt" Feature to the "Golden Share" to Resolve the SPS Convert/Cancel Debate?

A "Golden Share" with a "Contingent Value Receipt" feature would ensure Treasury gets an acceptable taxpayer return on GSE recap/release while maintaining fairness to GSE common stockholders

I have written previously at GSE Recap/Release: The Substance and Optics of Cancelling Treasury's Senior Preferred Stock in Exchange for a "Golden Share" that a Golden Share issued to Treasury in connection with a GSE recap/release could contain bespoke provisions designed to alleviate certain concerns the Trump 47 administration might have about a GSE recap/release.

One concern discussed in that post was whether the Trump 47 administration could maintain a desired level of control over the GSEs for some time after conservatorship release.

The Golden Share could contain a supermajority voting provision that could last as long as Trump 47 would desire. It could expire at the end of the Trump 47 administration, or continue (assuming a successor POTUS was elected that met Trump 47’s approval) until terminated by that successor POTUS.

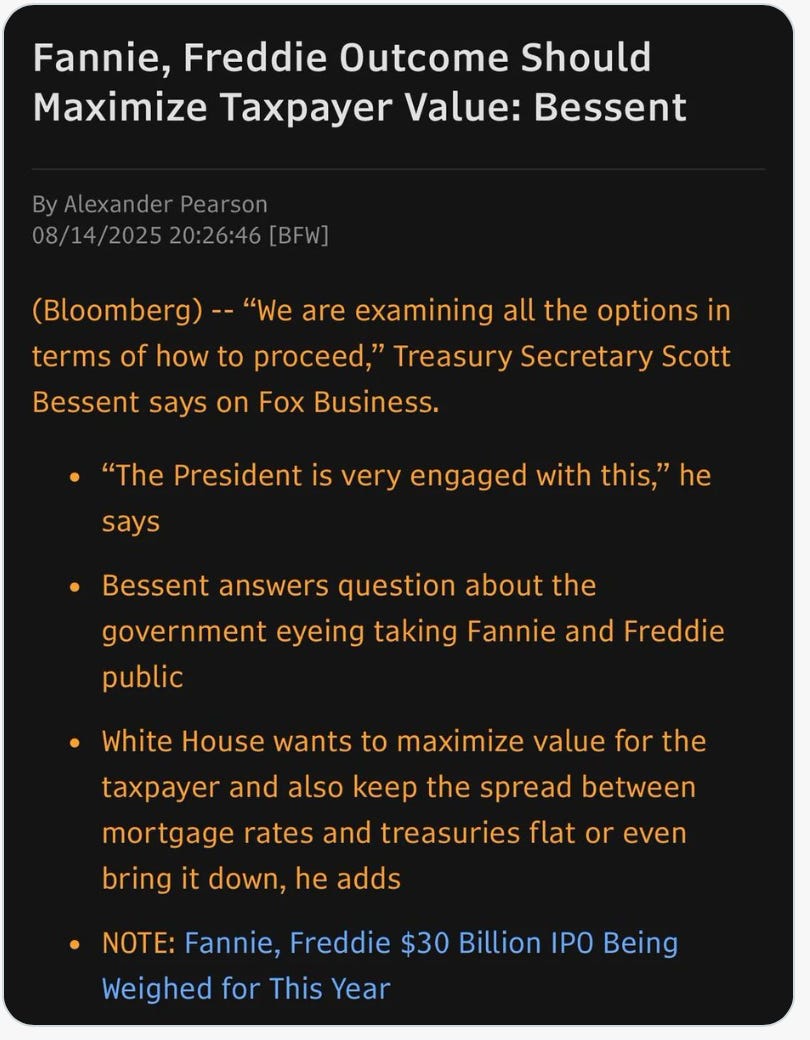

Another concern might be whether the terms of the GSE recap/release would provide US taxpayers an acceptable financial return on Treasury’s investment in the GSEs. For example, see the following Bloomberg note published on X today:

When investors consider how Treasury might “maximize value for the taxpayer” in connection with a GSE recap/release, immediately the question arises whether Treasury will convert into common stock or cancel all or some of its senior preferred stock liquidation balance (SPS).

I have focused on a normative reason for cancellation in GSE Recap/Release: HERA's "Best Interest" Provision is a Two-Way Ratchet. Obama Administration Used It To Destroy GSE Shareholder Value. Trump 47 Can "Reverse The Ratchet" in a GSE Recap/Release.

The Obama Net Worth Sweep was a fraudulent and disgraceful financial transaction that economically nationalized the GSEs and caused financial loss for many GSE shareholders (who could well be current MAGA supporters). By canceling the SPS, Trump 47 would end once and for all after 13 years the continuing malign effect of this Obama administration financial scandal.

Another question would focus on whether SPS cancellation or conversion would provide Treasury the larger economic return.

While one might think conversion into additional common stock would provide an additional return for Treasury, this would result in a massive dilution of existing common stockholders but provide only a 20.1% fully-diluted increment to Treasury’s shareholding (since Treasury is already a 79.9% shareholder by virtue of its warrants).

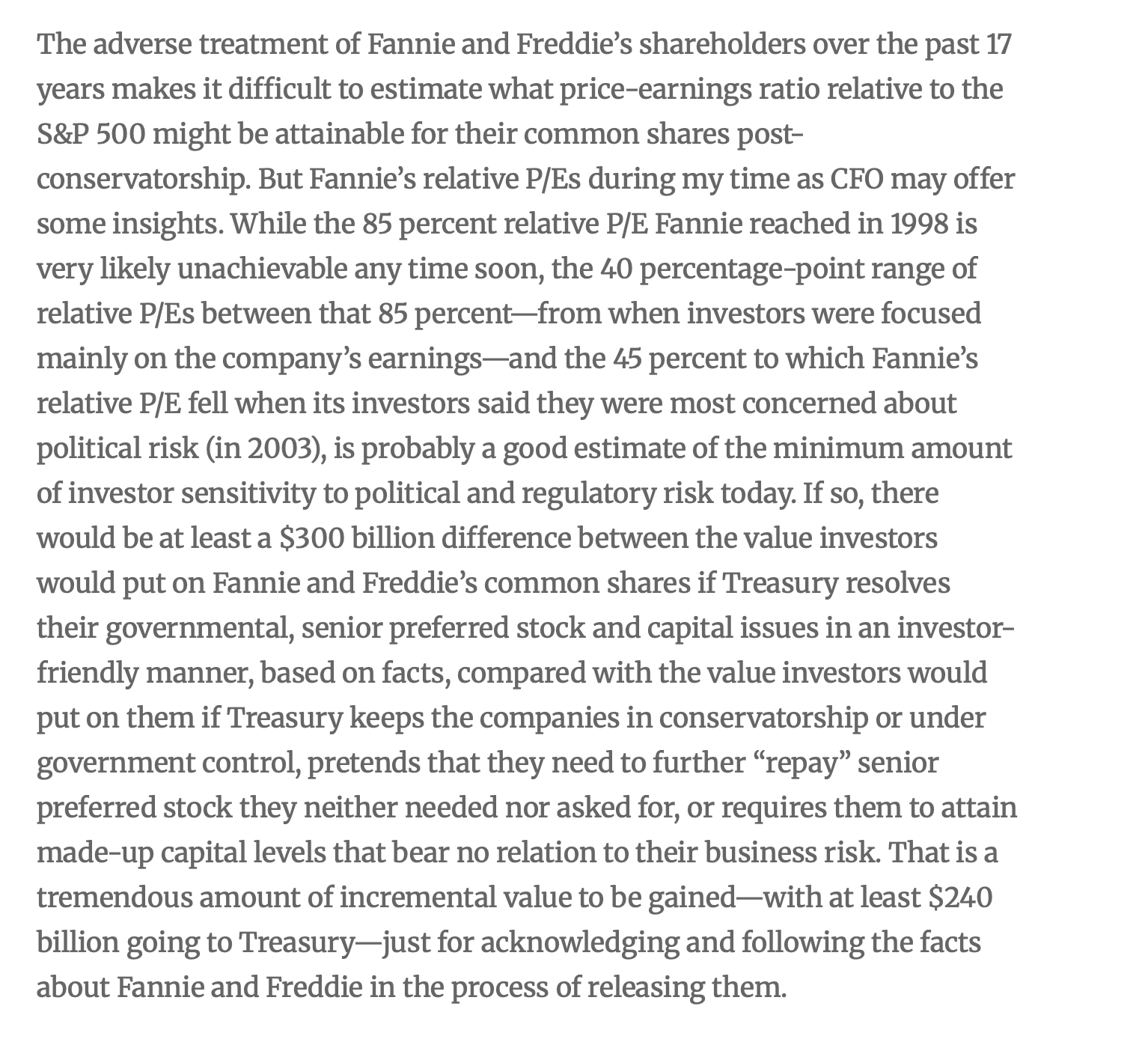

Tim Howard has pointed out in a blog post entitled A Matter of Facts that the P/E multiple for GSE common stock is highly variable and dependent on matters of market perception that go well beyond forecasted earnings. Mr. Howard cogently argues that Treasury’s return from cancelling the SPS would exceed that from converting the SPS into common stock because the market would assign a depressed P/E multiple in the case of conversion.1

I have been in many financial transactions where “leaving something on the table” for counterparties proved to be the wiser course of action for the party with leverage.

But why make a binary choice between SPS cancellation and conversion ex ante when one can keep the choice somewhat open-ended, and resolvable ex poste in the future?

When there is a disagreement over valuation between parties to a transaction, there are various methods to bridge that valuation difference through financial instruments that determine part of the transaction’s valuation based upon future events.

For example, in the case of a license of new intellectual property (IP) to be granted by the inventor to a business which will commercialize the IP, the standard way to bridge valuation differences is to incorporate an “earn-out” provision which incentivizes the business to commercialize but also provides some additional upside for the inventor.

You see contingent value receipts (CVRs) issued by acquiring companies to acquired company shareholders to bridge a valuation difference relating to the value of the acquired company. The CVRs will bloom into value for the acquired company shareholders if the acquired company’s financial metrics blossom after acquisition.

Something similar could be done in connection with a GSE recap/release.

In the Golden Share that Treasury would receive in connection with a GSE recap/release, there could be provision for a CVR that could provide Treasury additional value if Treasury has not achieved a specified monetary return (or unrealized gain if its shares are not sold) from its 79.9% common stock holding within a specified period of time.

Would this CVR feature of a Golden Share affect the trading price of the outstanding GSE common stock? Perhaps if the GSE common stock languishes in price; likely not if the GSE common stock trades at a value likely to provide Treasury its desired return from its base 79.9% common stock holding.

[This is a free post available to all without paywall. If you value my work, I would encourage you to become a paying subscriber]

* * * * *

As always, this substack provides investment analysis, not investment advice. Do your own due diligence.

From Tim Howard’s blog post:

I like the Golden Share and but would this get us arround legal concerns?

Also, can we confidently say that Bissent is holding the keys on the restructuring agreement and how it unfolds?

Or will it be Calabria, a Cato Institute bureaucrat, who oeversees the WH Office of Management and helped write the SPSA and the whispered 'Minuchin Dilution Solution' SPSA exit plan sitting on the shelf.

Pulte will also have a voice here, but I think he differs to Trump and Bissent and they are both big-bang buys who will want this to look big and shiny!

My 2-cents are that they erase some or all of the SPS and go for the Big-Bang to trumpet their win!

Would there be any legal pushback is they erased the SPS, or part or went to the Golden Share? If so, who would the pushback come from?