If Treasury Doesn't Cancel the SPS in a GSE Recap/Release, Will GSE Shareholders Have a Second Breach of Implied Covenant of Fair Dealing NWS Case?

FHFA breached the implied covenant of fair dealing by entering into the Net Worth Sweep. Will FHFA expose GSEs to massive additional damages if Treasury doesn't cancel the SPS in a GSE recap/release?

If Treasury does not cancel its GSE senior preferred stock (SPS) in connection with a GSE recap/release, will FHFA once again breach its implied covenant of fair dealing and expose the GSEs to legal risk and potentially massive damages?

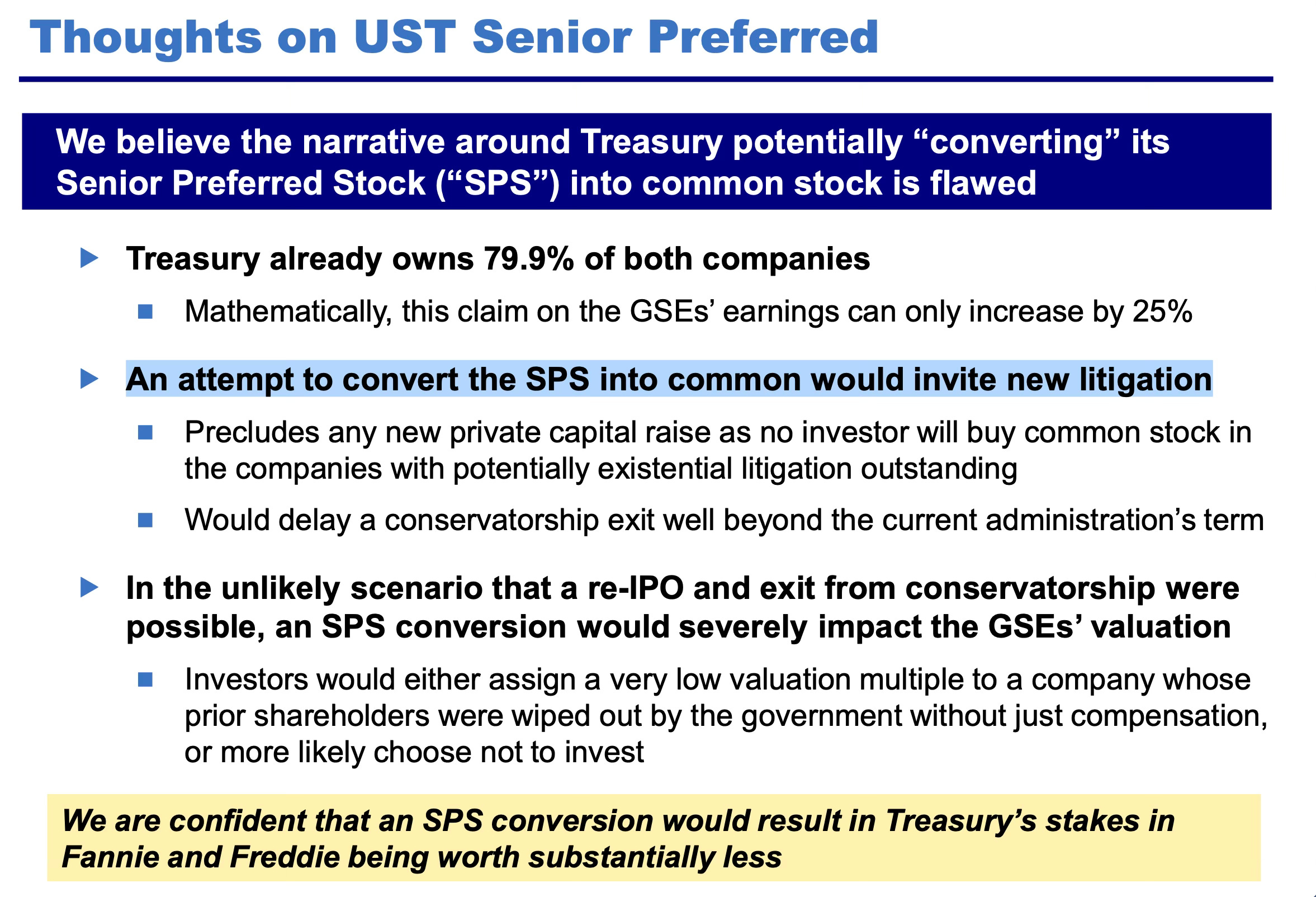

This is a question that was raised somewhat obliquely by Bill Ackman in his X slide deck, in which he posited that Treasury’s GSE warrants should be valued at approximately $300 billion in the event of a GSE recap/release on the terms he envisions. Under this scenario where Treasury cancels its SPS, GSE common stock would be valued at over $30 per share after two (in the case of FNMA) or three (in the case of FMCC) years.

Ackman at p.97 of the slide deck states that “[a]n attempt to convert the SPS into common would invite new litigation.”

In this post, I consider the potential for this new litigation.

This new litigation would “piggyback” on the existing breach of implied covenant of fair dealing case (In re Fannie Mae/Freddie Mac Senior Preferred Stock Purchase Agreement Class Action Litigations). In the existing case, FHFA as conservator (and thus the GSEs) was found liable to the plaintiff GSE shareholders class for approximately $780 billion.1

This damage award resulted from FHFA’s breach of its implied covenant of fair dealing by entering into the Net Worth Sweep (NWS) with Treasury. While FHFA as conservator breached the covenant, the GSEs would have to pay the judgment.

This jury verdict was based upon evidence presented at trial as to whether the plaintiff class GSE shareholders’ suffered “lost value” in connection with the NWS.2

The current legal posture of In re Fannie Mae/Freddie Mac Senior Preferred Stock Purchase Agreement Class Action Litigations is that Judge Lamberth has affirmed the jury verdict over FHFA’s motion to overturn the verdict. It is expected that FHFA will appeal.

I have previously written about the caselaw regarding the implied covenant of fair dealing, and I expect the DC Court of Appeals would not reverse the judgment if it is appealed.

Judge Lamberth also held that the breach claim ran with the shares, so that evidence for the entire period from the NWS through trial could be presented as to whether current GSE shareholders suffered economic loss from the NWS.

I examine below the paywall whether Treasury may expose FHFA, and thus the GSEs, to as much as $41 billion of additional damages (using Ackman’s values) in the event FHFA agrees to have Treasury’s SPS converted into GSE common stock (as opposed to cancelled) in any GSE recap/release.

This SPS conversion would, in effect, be the “closing transaction” to that of entering into the NWS, and should likewise be found to be either another breach, or a continuation of the initial breach, of the implied covenant of fair dealing.

Keep reading with a 7-day free trial

Subscribe to Rule of Law Guy’s Newsletter to keep reading this post and get 7 days of free access to the full post archives.